Unlocking Accuracy: The Power Of Positive Controls For Process Verification

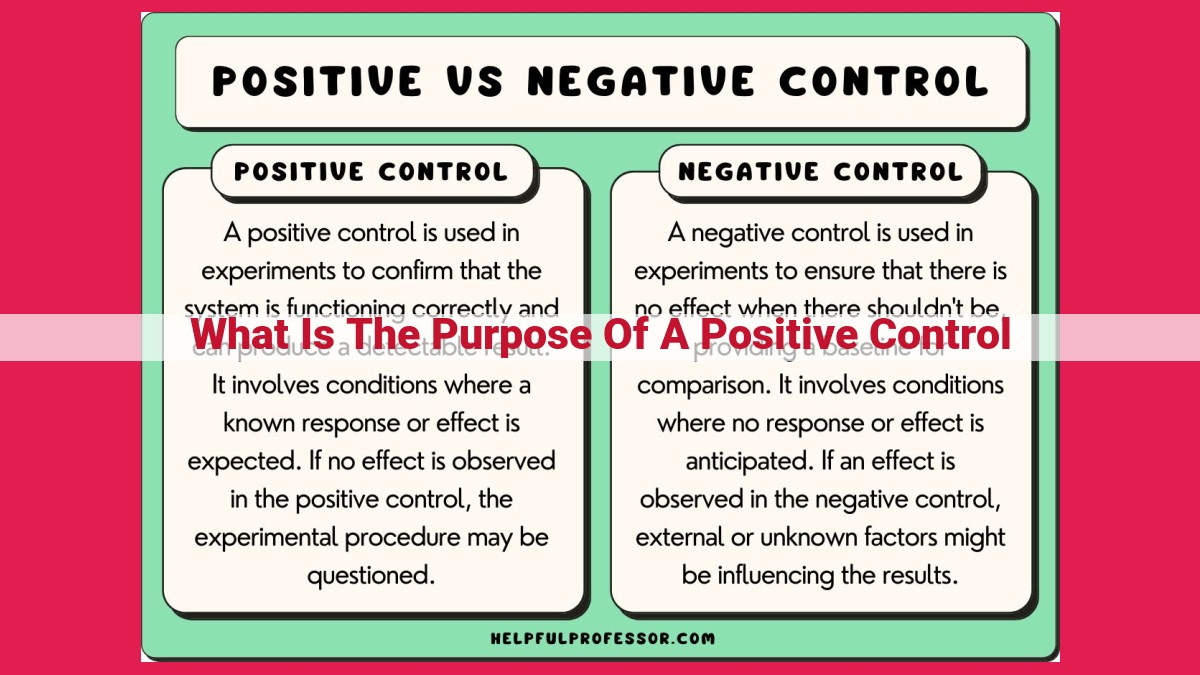

Positive controls serve as known values in a process to verify accuracy. They help ensure that control mechanisms are functioning properly and that desired results are being achieved. By comparing actual outcomes to known values, positive controls identify potential errors or deviations from expected outcomes, maintaining system accuracy and preventing misinterpretations.

Unveiling the Power of Controls: Ensuring Accuracy and Preventing Errors

In the realm of finance and scientific research, where precision and reliability are paramount, controls play an indispensable role. They act as vigilant guardians, safeguarding valuable assets, deterring fraudulent activities, and ensuring the seamless flow of accurate information.

The Importance of Internal and External Controls

Within organizations, internal controls establish a framework of policies, procedures, and mechanisms that govern financial operations. These controls, meticulously designed by management, serve as a robust defense against theft, embezzlement, and other financial malpractices. By segregating duties, implementing authorization protocols, and maintaining accurate accounting records, internal controls foster a culture of accountability and compliance.

External controls, on the other hand, provide an independent assessment of an organization’s financial health. External auditors, armed with their expertise and objectivity, conduct thorough audits to verify the accuracy of financial statements, evaluate the effectiveness of internal controls, and ensure compliance with regulatory requirements. Their watchful eyes bring to light discrepancies and potential weaknesses, contributing to the overall credibility and transparency of financial reporting.

Internal Control Concepts

- Define independence, materiality, and risk assessment, and explain their role in internal control systems.

Understanding Internal Control Concepts: A Foundation for Accurate Reporting

Internal controls are the cornerstone of any organization’s financial reporting system, safeguarding assets, preventing fraud, and ensuring accuracy. These controls are not merely a bureaucratic burden but rather a crucial element in maintaining the integrity and reliability of financial data.

At the heart of internal controls lies the concept of independence. This means that individuals involved in the financial reporting process must be free from conflicts of interest that could compromise their objectivity. By maintaining independence, organizations can prevent biased or inaccurate reporting and protect the interests of stakeholders.

Another key concept is materiality. This refers to the significance of an error or omission in financial statements. Materiality is subjective and depends on the nature and size of the organization. By establishing materiality thresholds, organizations can focus their control efforts on items that have the potential to materially distort financial results.

Finally, risk assessment is essential in designing an effective internal control system. Organizations must identify and evaluate the risks that could threaten the accuracy of financial reporting. This involves considering both internal factors (such as employee fraud) and external factors (such as economic downturns). By understanding potential risks, organizations can tailor their controls to mitigate these threats.

These three concepts—independence, materiality, and risk assessment—form the foundation of internal control systems. By embracing these principles, organizations can create a control environment that enhances the reliability of financial reporting, protects against errors and fraud, and ultimately builds trust among stakeholders.

External Control Mechanisms: Ensuring Trust and Compliance

External auditors play an indispensable role in the financial world, acting as the guardians of accuracy and compliance. Their meticulous audits provide independent assurance that financial statements fairly represent an organization’s financial health and adhere to established regulations.

By performing thorough examinations of financial records, external auditors identify potential errors or irregularities. They evaluate internal control systems, assess compliance with accounting principles, and uncover any instances of fraud or mismanagement. Their objective perspective and rigorous methodologies ensure that financial statements are reliable and trustworthy.

Moreover, external auditors play a crucial role in ensuring compliance with laws and regulations governing financial reporting.** They verify that organizations adhere to industry standards and follow established accounting guidelines. This safeguards the interests of investors, creditors, and other stakeholders who rely on financial statements for decision-making.

In essence, external auditors act as a bulwark against financial misconduct and error. Their independent scrutiny and rigorous procedures contribute to the integrity and credibility of financial reporting, fostering trust in the financial markets and protecting the interests of all stakeholders.

The Essential Role of Controls in Maintaining Accuracy and Preventing Errors

In the realm of accounting, internal and external controls are the gatekeepers of financial integrity. Positive Controls act as proactive guardians, ensuring that every transaction is meticulously authorized, recorded, and reconciled. They guarantee the accuracy of financial data by following predefined procedures and verifying the validity of information.

On the other hand, Negative Controls play a detective role, scrutinizing financial records for anomalies and unauthorized activities. By detecting errors, preventing fraud, and protecting against financial losses, they serve as a robust line of defense against unethical practices.

Experimental Controls venture into the realm of scientific research, providing a structured framework for testing hypotheses and establishing cause-and-effect relationships. They meticulously measure and analyze data to control for variables and ensure the validity of experimental findings.

Striking a Balance: Control Groups and Treatment Groups

In scientific experiments, Control Groups act as the benchmark against which the effects of an experimental intervention are compared. They receive no treatment, allowing researchers to isolate the impact of the experiment on the Treatment Groups. Randomization is employed to minimize bias and ensure that both groups are representative of the population being studied.

Blinding and Randomization: Ensuring Objectivity

Blinding eliminates bias by keeping participants and researchers in the dark about which group they belong to. Randomization further enhances objectivity by ensuring that participants are assigned to groups randomly, reducing the risk of systematic errors.

The Power of Placebos

In clinical trials, Placebo Groups play a critical role in controlling for psychological factors. By administering a placebo (an inactive substance), researchers can effectively isolate the effects of the actual treatment, ensuring that positive outcomes are not due to expectations or other biases.

The Gold Standard of Clinical Evidence: Randomized Controlled Trials (RCTs)

RCTs represent the pinnacle of clinical evidence, providing the highest level of confidence in the efficacy of a treatment. By randomly assigning patients to treatment and control groups, blinding participants and researchers, and employing strict protocols, RCTs minimize bias and produce results that are both reliable and generalizable.

Control Groups vs. Treatment Groups: The Foundation of Scientific Experimentation

In the realm of scientific research, control groups and treatment groups play pivotal roles in unraveling the cause-and-effect relationships that shape our world. These groups form the backbone of experiments, providing a baseline for comparison and ensuring the validity of the findings.

Control groups serve as the benchmark against which the effects of an experimental intervention are measured. They receive no special treatment or intervention, allowing researchers to establish a baseline response or outcome. By comparing the results of the treatment group with the control group, scientists can determine whether the intervention has a measurable effect.

Treatment groups, on the other hand, receive the experimental intervention that is being tested. These groups are subjected to the independent variable (the factor being manipulated) and are closely monitored to observe the dependent variable (the factor being measured). The comparison between the treatment and control groups helps researchers determine whether the intervention has a causal effect on the dependent variable.

In designing experiments with control and treatment groups, randomization plays a crucial role. Random assignment of participants to each group ensures that any differences in outcomes are not due to inherent differences between the groups. This minimizes bias and strengthens the validity of the experimental results.

Blinding and Randomization for Control

- Blinding: Explain its purpose in eliminating biases and maintaining objectivity.

- Randomization: Describe its importance in minimizing bias and ensuring the validity of experimental results.

Blinding and Randomization: Ensuring Impartiality and Validity in Research

In the realm of scientific research, blinding and randomization are indispensable tools that help researchers control for biases and ensure the validity of their results.

Blinding: Unmasking the Deception

Blinding involves concealing the identity of the study group to which participants belong. This strategy aims to eliminate biases that might arise if participants or researchers know the treatment they are receiving or administering. By keeping all parties in the dark, blinding helps maintain objectivity and prevents preconceived notions from influencing the study’s outcome.

Randomization: The Art of Chance Distribution

Randomization is the act of randomly assigning participants to different study groups. This technique serves two key purposes. First, it minimizes selection bias—the possibility that certain participant characteristics, such as age or health condition, could influence the study’s results. Randomization ensures that both treatment and control groups are representative of the larger population.

Second, randomization helps control for confounding factors. These are variables that may affect the study’s outcome but are not the focus of the research question. By randomly distributing participants across groups, randomization reduces the likelihood that any one confounding factor will disproportionately influence the results.

Blinding and Randomization in Action

Blinding and randomization are often used in clinical trials, where researchers aim to determine the effectiveness of new medical treatments. In a double-blind clinical trial, for example, neither the participants nor the researchers know which treatment (experimental or placebo) the participants are receiving. This design helps prevent the placebo effect—the psychological response that can influence study outcomes when participants know they are receiving a treatment.

Blinding and Randomization: The Cornerstones of Scientific Integrity

Blinding and randomization are fundamental to scientific research because they enhance the validity and reliability of study results. By minimizing biases and controlling for confounding factors, these techniques ensure that the conclusions drawn from the research are accurate and unbiased.

Therefore, when evaluating scientific studies, it is crucial to consider the extent to which blinding and randomization were employed. These techniques provide a solid foundation for trustworthy research findings that can inform decision-making and advance our understanding of the world.

The Significance of Placebo Groups in Clinical Trials

In the realm of medical research, clinical trials play a crucial role in testing the effectiveness and safety of new treatments. At the heart of these trials lies the placebo group, a vital component that ensures unbiased and reliable results.

A placebo group is a control group that receives a dummy treatment, such as a sugar pill or saline solution. Its primary purpose is to control for the psychological effects of receiving a treatment, known as the placebo effect. This effect can influence participants’ perception of their symptoms and response to the treatment.

By comparing the outcomes of the placebo group to those of the group receiving the actual treatment, researchers can isolate the effects of the treatment itself. This allows them to determine whether the observed improvements are due to the treatment or to other factors, such as participant expectations.

Placebo groups also serve as a baseline for comparison. They provide a reference point against which the effectiveness of the treatment can be measured. By contrasting the outcomes of the placebo group with those of the treatment group, researchers can quantify the true effect of the treatment and draw valid conclusions.

In clinical trials, masking or blinding is often used to eliminate biases that can compromise the validity of the results. Blinding ensures that neither the participants nor the researchers know which group a participant is assigned to. This helps to prevent both participants and researchers from being influenced by their subjective beliefs or expectations.

The use of placebo groups in clinical trials is essential for ensuring the credibility and reliability of the findings. By controlling for psychological effects and providing a baseline for comparison, placebo groups enable researchers to accurately assess the effectiveness of treatments and advance the field of medicine.

The Gold Standard in Clinical Research: The Randomized Controlled Trial (RCT)

When it comes to evaluating new medical treatments, Randomized Controlled Trials (RCTs) reign supreme as the gold standard. RCTs are renowned as the most rigorous type of clinical trial, providing the highest level of evidence that a particular intervention is truly effective.

An RCT involves randomly assigning participants into two groups: the control group and the treatment group. The control group receives either a placebo (a harmless substance that resembles the treatment) or a standard care treatment, while the treatment group receives the new treatment or intervention being studied.

The randomization process plays a crucial role in minimizing bias and ensuring that the two groups are similar in all other respects. This allows researchers to compare the outcomes between the two groups and confidently conclude whether the new treatment is more effective than the control.

RCTs are particularly valuable for establishing causal relationships between a treatment and an outcome. By controlling for other factors that could influence the outcome, RCTs provide strong evidence that the observed effect is due to the treatment itself.

For example, an RCT might compare the effectiveness of a new drug for treating a specific disease to a placebo. If the drug group shows significantly better outcomes than the placebo group, researchers can conclude that the drug is indeed effective in treating the disease.

RCTs are essential for advancing medical knowledge and improving patient care. They provide the most reliable evidence on which physicians can base their treatment decisions, ensuring that patients receive the best possible care.