Understanding Socially Optimal Quantity: Maximizing Economic Efficiency

The socially optimal quantity is the point at which the marginal cost of production equals the marginal benefit to consumers. To find this quantity, we compare the supply curve (showing the relationship between production and marginal cost) with the demand curve (showing the relationship between consumption and marginal benefit). The optimal quantity is where these two curves intersect. Government intervention may be required to correct market failures that prevent the market from reaching the social optimum, such as externalities or lack of property rights. Achieving the social optimum maximizes economic well-being by ensuring efficient resource allocation and minimizing deadweight loss.

Defining Socially Optimal Quantity

- Explain the concept of social optimum as the point where marginal benefit equals marginal cost.

Defining Socially Optimal Quantity: The Economic Balancing Act

In the realm of economics, there’s an elusive concept known as the socially optimal quantity that holds the key to efficient resource allocation. It’s a point of equilibrium where the marginal benefit (the additional benefit gained from producing one more unit) equals the marginal cost (the additional cost incurred from producing that same unit).

Imagine a hypothetical market for artisanal coffee. Every sip of coffee brings a bit of bliss to the consumer, but each additional cup also requires more resources and effort to produce. As more coffee is produced, the marginal benefit decreases while the marginal cost increases. The socially optimal quantity is that sweet spot where these two forces meet.

Importance of Social Optimum: Ensuring Efficiency and Minimizing Waste

Achieving the socially optimal quantity is crucial for maximizing economic well-being. When production is below this point, undersupply occurs, and society misses out on potential benefits. But when production exceeds the optimum, oversupply results, leading to wasted resources and potential losses.

The socially optimal quantity promotes efficient resource allocation. It ensures that the available resources are utilized in a way that generates the greatest overall benefit for society. Any deviation from this point can lead to market failures and inefficient outcomes that harm the economy.

Key Concepts for Understanding Social Optimum

To fully grasp the concept of social optimum, we need to delve into four key pillars: marginal cost, production, marginal benefit, and consumption.

Marginal Cost (MC): This is the additional cost incurred when producing one more unit of a good or service. In other words, it’s the change in total cost caused by a one-unit increase in output.

Production: The process of creating goods or services using resources such as capital, labor, and raw materials. The relationship between production and MC is crucial as it determines the total cost of producing a given output.

Marginal Benefit (MB): The additional benefit gained from consuming one more unit of a good or service. This concept is subjective and depends on individual preferences and needs.

Consumption: The act of using goods and services to satisfy wants. Understanding consumption patterns is essential for determining the demand for a particular good or service, which in turn influences its production and market price.

These four concepts are interconnected and influence the determination of the socially optimal quantity. The goal is to find a point where the marginal benefit of producing one more unit just equals the marginal cost of producing that unit. This equilibrium represents the optimal allocation of resources and maximizes societal well-being.

Reaching Social Optimum: Efficiency and Deadweight Loss

- Explain how social optimum leads to efficient resource allocation and define deadweight loss.

Reaching Social Optimum: Efficiency and Deadweight Loss

In the pursuit of economic efficiency, the concept of socially optimal quantity plays a pivotal role. This is the ideal point where the marginal benefit (MB) of an economic activity equals its marginal cost (MC). When this equilibrium is achieved, society allocates resources effectively, maximizing total welfare.

Efficient Resource Allocation

At the social optimum, resources are channeled towards their most valuable uses. Producers are incentivized to supply the optimal quantity of goods or services, as they can reap maximum profits when MB=MC. Consumers, in turn, benefit from lower prices and greater access to goods that provide the highest marginal utility.

Deadweight Loss

Deviation from the social optimum results in deadweight loss, a reduction in societal well-being due to inefficient resource allocation. This loss manifests in two ways:

- Overproduction: When output exceeds the social optimum (MB<MC), resources are wasted on producing goods or services that consumers don’t value as much.

- Underproduction: When output falls short of the social optimum (MB>MC), society fails to produce goods or services that would have provided net benefits to consumers.

Consequences of Deadweight Loss

Deadweight loss has severe economic consequences:

- Reduced economic growth: Suboptimal resource allocation stifles innovation and productivity.

- Higher prices for consumers: Inefficient supply leads to higher production costs, passed on to consumers in the form of higher prices.

- Diminished consumer welfare: Overproduction leads to excess supply and potential waste, while underproduction denies consumers access to goods and services that would enhance their lives.

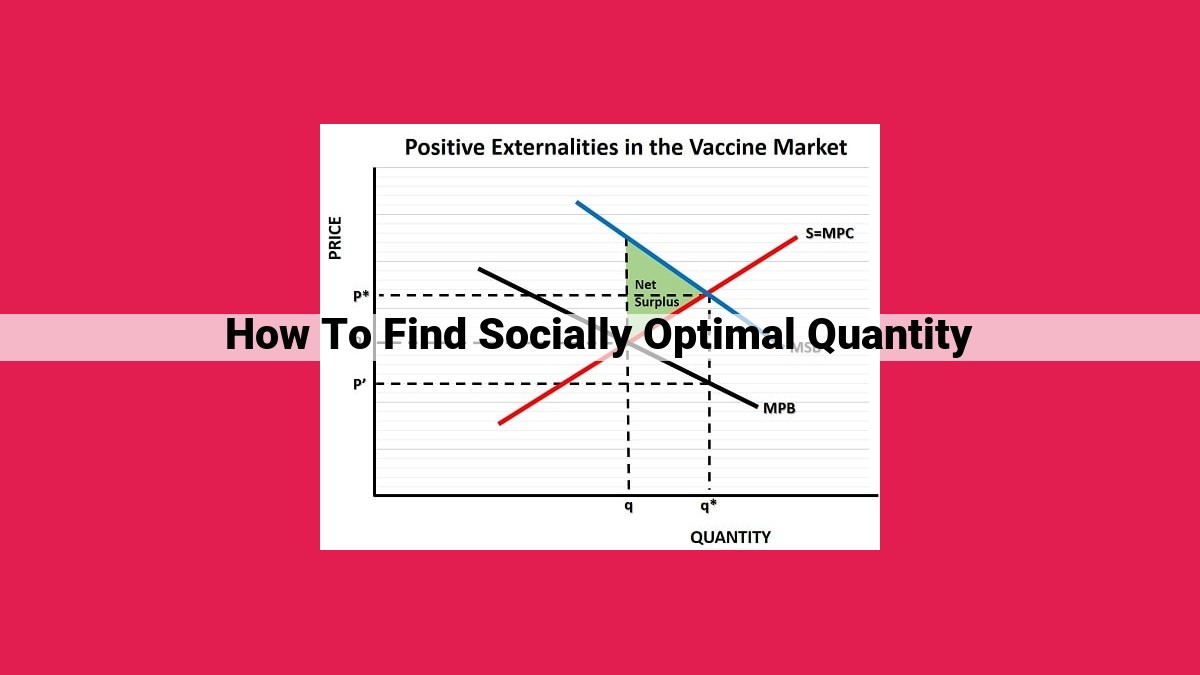

Property Rights and Externalities

- Describe the role of property rights in shaping production and consumption incentives.

- Discuss how externalities can lead to market failures and deviation from social optimum.

Property Rights and Externalities: Shaping Production, Consumption, and Market Failures

Property rights play a crucial role in shaping the incentives for production and consumption. Clear and well-defined property rights allow individuals to own and control resources, which influences their decisions regarding production and consumption. For instance, a farmer with strong property rights over their land has the incentive to invest in its productivity, knowing that they will reap the benefits of their efforts. Conversely, in the absence of clear property rights, individuals may hesitate to invest in resources or may overexploit them, leading to inefficiencies.

Externalities are another factor that can affect the social optimum. Externalities occur when the actions of one party have unintended consequences on another party. For example, a factory emitting pollution into the air creates a negative externality for nearby residents, affecting their health. On the other hand, a park provides a positive externality, enhancing the well-being of those living in the area.

Externalities can lead to market failures. In the case of negative externalities, the private marginal cost (the cost to the producer) is less than the social marginal cost (the cost to society, including the externality). This can result in overproduction, as producers do not consider the full costs of their actions.

Similarly, with positive externalities, the private marginal benefit (the benefit to the producer) is less than the social marginal benefit (the benefit to society, including the externality). This can lead to underproduction, as producers do not fully recognize the value of their actions.

Understanding the role of property rights and externalities is crucial for achieving social optimum. By considering the impact of externalities and establishing appropriate property rights, we can create incentives that encourage efficient resource allocation and prevent market failures.

Determining the Socially Optimal Quantity: A Roadmap to Economic Harmony

In the realm of economics, where efficiency and well-being dance harmoniously, the concept of social optimum reigns supreme. It represents the sweet spot where marginal benefit (the additional value gained from consuming one more unit) equals marginal cost (the additional cost of producing that extra unit). Reaching this optimal point is crucial for achieving a society’s economic aspirations.

Unveiling the Steps to Social Optimum

Determining the socially optimal quantity involves a meticulous process of analysis and understanding:

1. Embrace the Marginal Cost Curve:

The marginal cost curve illustrates the additional cost incurred when producing each additional unit of a product. Understanding this curve is paramount as it reflects the true economic cost of production, considering both explicit costs (direct expenses) and implicit costs (opportunity costs).

2. Charting the Marginal Benefit Curve:

The marginal benefit curve depicts the additional benefit or value gained by consumers when they purchase an additional unit of a product. This curve showcases consumers’ willingness to pay for each unit, which is crucial for determining the optimal quantity.

3. Equilibrium: Where Curves Intersect

The socially optimal quantity is the point where the marginal cost curve and the marginal benefit curve intersect. At this intersection, the additional benefit derived from consuming one more unit is precisely equal to the additional cost incurred in producing it.

4. Understanding Deadweight Loss

When market forces fail to reach social optimum, a situation known as deadweight loss occurs. This loss represents the difference between the socially optimal quantity and the actual quantity produced or consumed. It measures the economic inefficiency resulting from the deviation from the optimal point.

5. Redefining Equilibrium with Government Intervention

In instances where market failures impede the attainment of social optimum, government intervention may be necessary. This intervention aims to correct market distortions, such as externalities or missing property rights, to nudge the economy towards the socially optimal quantity.

Government Intervention for Efficiency

Understanding Market Failures

In a perfectly competitive market, the forces of supply and demand naturally lead to an efficient allocation of resources and a level of output that maximizes economic welfare. However, real-world markets often experience market failures, which occur when the private market outcome deviates from the socially optimal outcome. Market failures can arise due to various reasons, such as externalities, monopolies, or information asymmetries.

Role of Government Intervention

When market failures occur, government intervention may be necessary to correct these inefficiencies and promote social optimum. Government intervention can take various forms, depending on the specific market failure being addressed.

One common form of intervention is public regulation, such as setting price ceilings or floors to address market power or price distortions. For example, price ceilings may be imposed to protect consumers from excessive prices in natural monopolies.

Another form of intervention is fiscal policy, such as taxes or subsidies, to encourage or discourage certain activities. For example, a Pigouvian tax can be imposed to internalize the negative externalities of a particular activity, such as pollution.

Achieving Social Optimum

Government intervention aims to align private incentives with social objectives and achieve social optimum. This involves setting the appropriate policies and regulations to maximize economic efficiency and minimize deadweight loss.

Benefits of Social Optimum

Achieving social optimum brings numerous benefits for the economy. It leads to a more efficient allocation of resources, increased production, lower prices, and higher consumer surplus. Ultimately, social optimum promotes economic well-being and enhances the overall quality of life for society.

The Paramount Importance of Socially Optimal Quantity for Economic Prosperity

Achieving the elusive state of social optimum is a pivotal pillar for fostering the economic well-being of society. It’s a point where the scales are balanced, with the equilibrium of marginal benefit and marginal cost leading to the optimal allocation of resources.

By aligning production and consumption, social optimum ensures that society’s needs are met with minimum waste and maximum efficiency. Such prudent resource management leads to increased productivity, lower costs, and an overall expansion of economic growth.

Moreover, it curbs the detrimental effects of deadweight loss, the gap between socially optimal output and actual production. By eliminating inefficiencies, social optimum maximizes societal welfare and unlocks opportunities for sustained economic prosperity.

In a nutshell, achieving social optimum is the keystone of economic vitality. It paves the way for industries to flourish, innovation to thrive, and citizens to reap the rewards of a thriving economy. Embracing this principle is not merely a theoretical pursuit but a fundamental ingredient for the long-term prosperity of any nation.