The Role Of Money In Streamlining The Circular Flow Model

Money streamlines the circular flow model by facilitating transactions through its roles as a medium of exchange, store of value, and unit of account. It enables specialization, reduces transaction costs, and promotes economic growth by supporting investment and capital formation. Money’s versatility ensures smoother and more efficient circulation of goods, services, and resources within the economy.

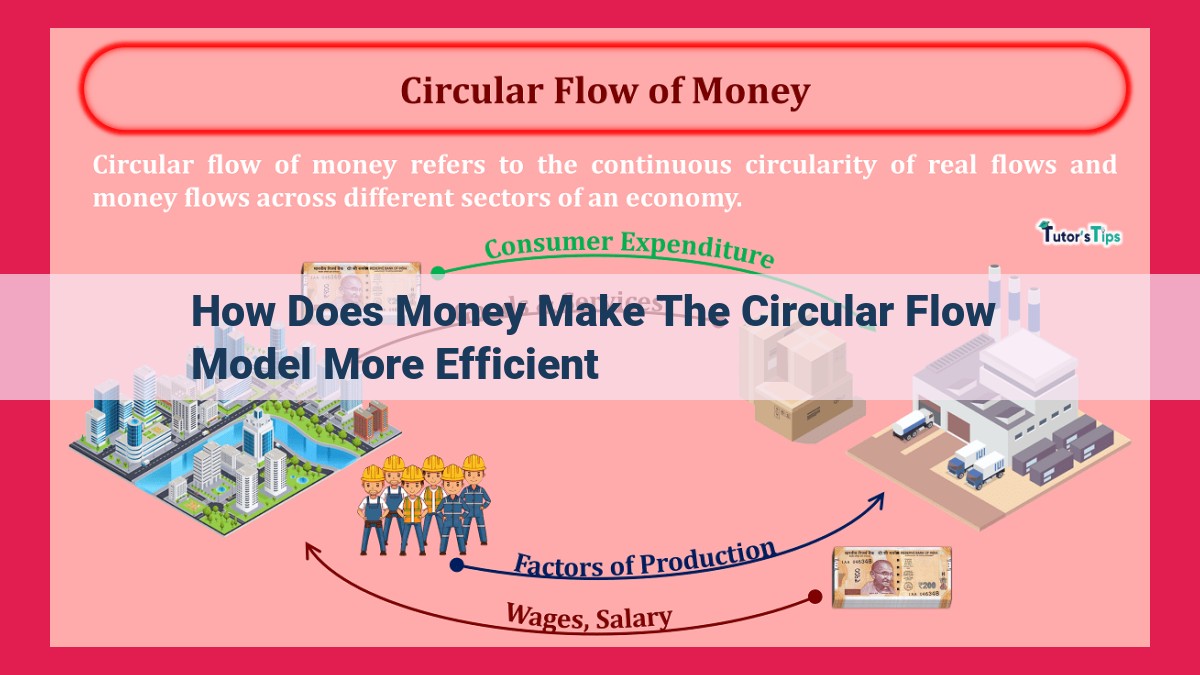

Money’s Role in the Circular Flow Model: A Journey Through Economic Transactions

In the realm of economics, the circular flow model is a visually compelling representation of the continuous flow of goods, services, and money within an economy. Money plays an indispensable role in this model, acting as the vital lubricant that facilitates economic transactions.

Imagine an economy as a vast marketplace, where individuals, businesses, and governments interact, exchanging products and services. Without money, this marketplace would resemble a chaotic barter system, where goods and services would be traded directly without a common medium of exchange.

However, the introduction of money transformed this marketplace into a highly organized and efficient system. Money became the medium of exchange, eliminating the need for cumbersome barter and allowing for seamless transactions between producers and consumers. Individuals could now purchase goods and services they desired, while businesses could sell their products and receive monetary compensation.

Furthermore, money serves as a store of value, allowing individuals to preserve their purchasing power over time. With money, people can save and invest, knowing that their financial assets will retain their value and can be used for future purchases. This storage function of money encourages saving and capital formation, which are crucial for economic growth.

In addition to its role as a medium of exchange and store of value, money also functions as a unit of account. It provides a common denominator for measuring the value of goods and services, enabling comparisons and facilitating economic decision-making. By establishing a common monetary standard, money simplifies price comparisons and allows for rational economic choices.

The presence of money also promotes specialization and trade. Individuals and countries can focus on producing what they do best and exchange their surpluses through monetary transactions. This division of labor and trade fosters comparative advantage, leading to greater overall production and economic efficiency.

Money reduces transaction costs by providing liquidity and a universal exchange rate. It eliminates the need for time-consuming and costly negotiations, making transactions faster and more convenient. In international trade, money reduces the complexity of exchange rates, facilitating global commerce.

Ultimately, money contributes to economic growth. It supports investment, capital formation, and productivity. When businesses and individuals have access to monetary resources, they can invest in technology, infrastructure, and human capital, which drives innovation, job creation, and overall economic expansion.

In conclusion, money’s multifaceted functions as a medium of exchange, store of value, unit of account, and facilitator of specialization, trade, and economic growth make it an indispensable component of the circular flow model. By providing a common means of transaction, preserving purchasing power, measuring value, and promoting efficiency, money plays a vital role in shaping and driving modern economies.

Money as a Medium of Exchange: Simplifying Transactions and Fostering Efficiency

In the realm of economics, money plays a crucial role as the primary medium of exchange. This fundamental function has revolutionized commerce by eliminating the complexities of barter systems, where goods and services were directly exchanged without the use of an intermediate medium.

Barter, while prevalent in rudimentary societies, posed significant challenges. Matching the needs and desires of two parties seeking to trade often proved arduous, leading to inefficient outcomes and limited economic growth. Money emerged as a solution to these inefficiencies, becoming a widely accepted and standardized means of payment that simplified transactions and lubricated the wheels of commerce.

By using money, individuals can purchase goods and services from others without the need to find someone who desires their own products or services in return. This eliminates the inefficiencies of barter and allows for a smooth flow of economic activity. For example, a farmer can sell their produce for money, which they can then use to purchase essential goods such as tools or clothing. The seller of those items, in turn, can use the money to acquire other necessities, and so on.

Moreover, money facilitates specialization and division of labor, as it allows individuals and societies to focus on producing goods and services in which they have a comparative advantage. Without money, it would be challenging to coordinate the exchange of goods and services across different regions or sectors of the economy.

In essence, money serves as a common denominator, enabling the valuation and exchange of a wide range of goods and services. Its existence simplifies transactions, reduces uncertainty, and promotes specialization, ultimately contributing to increased efficiency and economic prosperity.

Money as a Store of Value: Preserving Purchasing Power Over Time

In the realm of economics, money holds a crucial function as a store of value. By acting as a repository of purchasing power, money allows individuals and organizations to preserve their wealth over extended periods, enabling them to plan for the future and make informed financial decisions.

In the absence of money, individuals would need to rely on barter, exchanging goods and services directly. While this system sufficed in primitive societies, it becomes impractical as economies grow and specialize. Money, as a medium of exchange, simplifies transactions and eliminates the need for coincidence of wants, allowing individuals to store their wealth in a form that is universally accepted and easily convertible into other goods and services.

Money’s ability to store value also fosters savings and investment, which are vital for sustainable economic growth. By earning income, individuals can accumulate money and deposit it in banks or invest it in financial instruments that provide a return. This stored wealth serves as a buffer against unexpected expenses and allows individuals to plan for their future financial goals, such as retirement or education.

Furthermore, money’s role as a store of value facilitates capital formation. Investors can use their accumulated wealth to fund new businesses, purchase machinery, or expand existing operations. This capital investment drives innovation, technological advancements, and increased productivity, ultimately contributing to overall economic prosperity.

In conclusion, money’s ability to store value is a fundamental pillar of modern economic systems. It empowers individuals to preserve their purchasing power over time, facilitates savings and investment, and stimulates economic growth. By providing a secure and efficient medium for storing wealth, money enables individuals and economies to thrive and progress.

Money as a Unit of Account: The Yardstick of Economic Measurement

In the vast tapestry of economic activity, money emerges as a crucial element, fulfilling multiple roles that facilitate the smooth functioning of markets. One of its essential functions is as a unit of account, a universal yardstick that measures the value of goods and services.

Imagine a world without a standardized unit of value. Bartering, the exchange of goods directly for other goods, would dominate transactions. Determining the relative worth of different commodities would be a perplexing task, hindered by the complexities of comparing apples to oranges or wheat to livestock.

Money solves this problem by providing a common denominator. It assigns a numerical value to each good and service, enabling us to compare their worth objectively. This numerical representation simplifies decision-making, allowing individuals to evaluate the cost-benefit ratio of different purchases and prioritize their spending.

Moreover, as a unit of account, money facilitates price comparisons. By expressing prices in a common currency, it allows consumers to assess the relative affordability of similar products from different suppliers. This promotes competition among businesses and ensures that consumers receive the best value for their money.

Furthermore, money as a unit of account enables effective budgeting and long-term planning. Households and businesses can accurately track their expenses and income over time, creating a clear financial picture that supports informed decision-making. Governments also rely on money as a unit of account to track economic indicators such as GDP, inflation, and unemployment, which are essential for policy formulation.

In essence, money’s role as a unit of account is indispensable for a well-functioning economy. It establishes a common language of value that simplifies transactions, enables price comparisons, and supports informed economic decision-making. Without this standardized measure, the complexities of economic exchange would hinder progress and prosperity.

Money Facilitates Specialization and Trade

The advent of money has had a profound impact on the way we organize our economies. Before money, people had to rely on barter, a system of exchanging goods and services directly without using an intermediary. Barter is a cumbersome and inefficient way to do business, as it requires double coincidences of wants – that is, both parties in a transaction must have something that the other wants and vice versa.

Money solves the problem of double coincidences of wants by acting as a medium of exchange. Money is anything that is generally accepted as payment for goods and services. This means that people can specialize in producing goods and services that they are best at producing, and then use money to buy the goods and services that they need from others.

Specialization allows individuals and countries to produce more goods and services than they could if they had to be self-sufficient. This is because specialization allows people to focus on what they are best at, and to leverage the comparative advantages that they have. For example, a country that has a comparative advantage in producing wheat can specialize in producing wheat, and then use money to buy other goods and services that it needs from other countries.

Trade is the exchange of goods and services between individuals and countries. Trade is made possible by money, which allows people to compare the prices of goods and services, and to make decisions about how to allocate their resources. Trade allows countries to specialize in producing goods and services that they are best at producing, and to import goods and services that they cannot produce efficiently. This leads to a more efficient allocation of resources and a higher standard of living for everyone.

Money Reduces Transaction Costs

In the bustling marketplace of the economy, transactions are the lifeblood, connecting buyers and sellers in an intricate web of exchange. But these exchanges come with inherent costs, like the time and effort spent finding a suitable trade partner, verifying their trustworthiness, and negotiating terms. Enter money, the universal medium that streamlines these interactions, slashing transaction costs and greasing the wheels of commerce.

Liquidity, money’s ability to be easily converted into other goods or services, eliminates the need for barter, where goods are directly exchanged for other goods. This simplifies transactions, reducing the time and effort involved in finding someone who has what you want and wants what you have.

Exchange rates play a crucial role in facilitating international trade. By establishing a common unit of value, exchange rates allow individuals and businesses to compare the prices of goods and services across borders, ensuring that transactions are fair and minimizing the risks associated with currency fluctuations.

The cost-reducing power of money is undeniable. Its liquidity and exchange rates streamline transactions, making them faster, easier, and more efficient. This, in turn, lowers the barriers to trade, fosters specialization, and promotes economic growth. Money’s role as a transaction cost reducer is essential for a thriving and efficient economy.

Money Promotes Economic Growth

In the realm of economics, money plays a pivotal role in the growth and prosperity of nations. It is more than just a medium of exchange; it acts as the lifeblood of economic ecosystems, fueling investment, capital formation, and productivity, which ultimately drive economic expansion.

Investment and Capital Formation:

Money enables individuals and businesses to invest in productive assets, such as machinery, equipment, and research and development. Investments create new jobs, boost production capacity, and enhance technological advancements. By facilitating the flow of capital from savers to borrowers, money promotes capital formation, increasing business capacity and economic output.

Productivity and Innovation:

Money incentivizes innovation and productivity. Entrepreneurs and businesses are encouraged to invest in new technologies, products, and processes, knowing that they can reap the financial rewards. Money acts as a signal of value, allowing markets to allocate resources effectively, funding projects that generate the highest returns. As productivity increases, output grows, and the overall standard of living improves.

The Multiplier Effect:

When money is invested in the economy, it circulates and multiplies. New jobs are created in the production process, increasing wages and consumer spending. This spending stimulates further investment and job creation, leading to a positive multiplier effect. Money acts as the driving force in this virtuous cycle, accelerating economic growth.

Money’s role in promoting economic growth cannot be overstated. It facilitates investment, capital formation, and productivity, creating a thriving and prosperous economy. By understanding the intricate workings of money, policymakers can create an environment that fosters economic expansion and raises the standard of living for all.