Calculating Total Merchandise Purchase Costs: A Comprehensive Guide

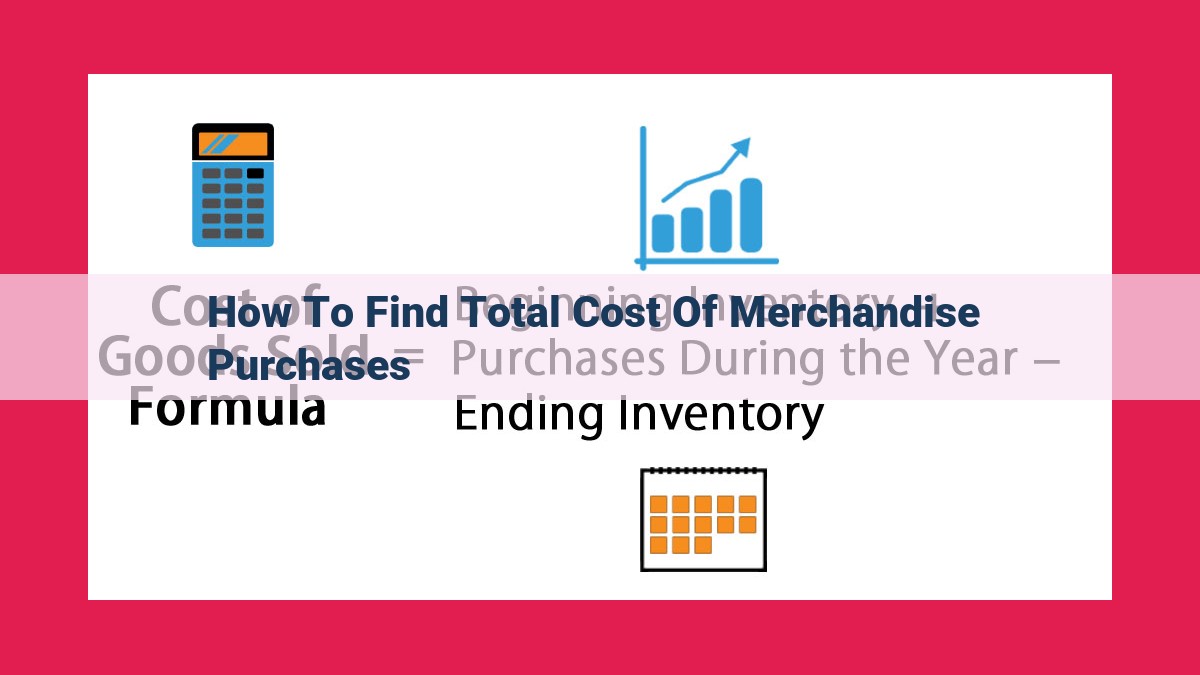

To determine the total cost of merchandise purchases, begin with the beginning inventory value. Add the cost of all purchases made during the period, including any transportation-in expenses. Calculate the ending inventory value and subtract it from the goods available for sale (beginning inventory + purchases + transportation-in) to arrive at the total cost of merchandise purchases. This calculation represents the cost of the goods that have been sold during the period.

Understanding Beginning Inventory: The Foundation of Inventory Management

When you embark on the journey of owning and operating a business that involves buying and selling merchandise, understanding the concept of beginning inventory is a crucial step. Beginning inventory refers to the stock of goods you have on hand at the start of a specific accounting period. It serves as the cornerstone for calculating the total cost of merchandise purchases during that period.

Imagine yourself as a business owner selling handmade crafts. At the beginning of January, you have 50 units of your signature product, each costing $10 to make. This means your beginning inventory for January is valued at $500.

Tracking Purchases Accurately: The Key to Inventory Management

In the realm of inventory management, accuracy reigns supreme. Tracking purchases accurately is not just a mundane task; it’s a strategic pillar upon which businesses thrive. Every dollar meticulously recorded ensures profitability and provides invaluable insights into the financial health of an organization.

Accurate purchase tracking allows businesses to maintain a real-time pulse on their inventory levels. It prevents overstocking, which can tie up capital and lead to spoilage. On the flip side, it also prevents understocking, which can result in lost sales and dissatisfied customers.

Moreover, accurate purchase data is essential for calculating the total cost of merchandise purchases. This figure, in turn, plays a crucial role in determining the cost of goods sold, which is a key determinant of a company’s gross profit. Misstated purchase costs can lead to inaccurate financial statements, misleading management, and potentially damaging decisions.

So, how do businesses ensure purchase accuracy? It begins with establishing clear internal controls. These controls should define the roles and responsibilities of personnel involved in the purchasing process, from requisition to payment. Robust controls prevent unauthorized purchases, promote timely recording, and provide a framework for reconciling purchase transactions with supplier invoices.

Additionally, investing in automated systems can significantly enhance purchase accuracy. Automated systems eliminate manual entry errors, streamline the approval process, and provide real-time visibility into purchase data. This allows businesses to identify and rectify discrepancies promptly, ensuring the integrity of their inventory records.

By regularly reviewing and reconciling purchase transactions, businesses can further strengthen their accuracy. Matching purchase orders, receiving reports, and vendor invoices provides an additional layer of verification and helps identify any potential errors or fraud. This diligence ensures that every dollar spent on merchandise is accounted for and contributes to a true and fair representation of a company’s financial performance.

Remember, accurate purchase tracking is not merely a compliance issue; it’s a foundation for sound business decisions. By investing in robust controls, embracing automation, and fostering a culture of accuracy, businesses can establish a solid footing for sustainable growth and profitability.

Considering Transportation Costs in Merchandise Purchase Calculations

Beyond the direct costs of acquiring inventory, businesses must also factor in the transportation-in expenses incurred to deliver those goods to their warehouse or retail location. These costs, which may include shipping, trucking, and handling fees, form an integral part of the total cost of merchandise purchases.

Why Include Transportation Costs?

Adjusting for Transportation Costs ensures an accurate representation of the total cost of inventory. By incorporating these expenses, businesses can determine the actual cost of bringing merchandise into the company. This ensures proper valuation of inventory and accurate financial reporting.

Nature of Transportation Costs

Transportation costs generally fall into two categories:

- Inbound Freight: Costs associated with transporting goods from the supplier to the business’s premises.

- Intra-Company Freight: Costs incurred for transferring inventory between different company locations.

Regardless of the type, these costs are directly related to the acquisition of inventory and should be treated as part of the total cost of merchandise purchases.

Impact on Calculations

To calculate the total cost of merchandise purchases, transportation-in expenses are added to the cost of goods purchased. This adjustment ensures that the merchandise’s full cost is reflected in the financial statements.

Formula:

Total Cost of Merchandise Purchases = Cost of Goods Purchased + Transportation-in Expenses

By considering transportation costs in their merchandise purchase calculations, businesses can accurately determine the true cost of inventory and ensure the reliability of their financial reporting.

Calculating Ending Inventory

- Define ending inventory and explain why it’s subtracted from goods available for sale.

Calculating Ending Inventory

In the realm of inventory management, there’s an important concept known as ending inventory. It represents the unsold merchandise left over at the end of an accounting period. This inventory holds significance in determining the cost of goods sold and ultimately, the net income of a business.

Ending inventory is subtracted from goods available for sale because it reflects the portion of inventory that hasn’t yet been sold and, therefore, hasn’t contributed to revenue. By subtracting it, companies can calculate the total cost of merchandise sold during a specific period.

For instance, suppose a clothing store has a beginning inventory of 100 shirts at a cost of $10 each, and it purchased 50 additional shirts at the same cost during the month. This brings the total goods available for sale to 150 shirts. However, if the store sells 75 shirts during the same period, its ending inventory becomes 75 shirts.

The total cost of merchandise purchases for the period can then be calculated by multiplying the number of units purchased (50) by the cost per unit ($10), which gives us $500.

Understanding ending inventory is crucial for businesses to accurately track their inventory levels and determine their profitability. By carefully monitoring this metric, companies can optimize their inventory management practices and make informed decisions about purchasing and sales.

Determining Goods Available for Sale

In the realm of accounting for inventory, calculating Goods Available for Sale is a crucial step in understanding a company’s cost of goods sold. This calculation seamlessly blends together three key elements: beginning inventory, purchases, and transportation-in expenses.

Beginning inventory represents the value of unsold inventory at the start of an accounting period. It serves as the foundation for tracking the flow of goods throughout the period.

Purchases, on the other hand, capture the cost of all merchandise acquired during the period, excluding transportation costs. Accurately recording purchases is paramount as they form a significant portion of the total cost of goods sold.

Finally, transportation-in expenses encompass the costs incurred to move purchased merchandise from the supplier to the company’s store or warehouse. These expenses are often overlooked but play a vital role in determining the complete cost of inventory.

To calculate Goods Available for Sale, simply sum up beginning inventory, purchases, and transportation-in expenses. This calculation provides a comprehensive view of all goods that were available for sale during the period.

Calculating the Total Cost of Merchandise Purchases: A Comprehensive Guide

When running a business that involves buying and selling goods, accurately determining the total cost of merchandise purchases is crucial. This blog post will delve into the formula used to calculate this cost and explain its various components.

The total cost of merchandise purchases, abbreviated as TCM, is an essential number in a company’s income statement. It represents the total cost of all goods purchased during a period. This cost includes not only the purchase price of the goods but also any additional expenses incurred to acquire them.

The formula for calculating TCM can be expressed as follows:

TCM = Beginning Inventory (BI) + Purchases (P) + Transportation-in (TI)

Let’s break down each component:

- Beginning Inventory (BI): This refers to the value of goods on hand at the beginning of a period.

- Purchases (P): These are the costs incurred to acquire new merchandise during a period.

- Transportation-in (TI): This represents the costs associated with transporting merchandise from the supplier to the company’s warehouse.

It’s important to accurately record all of these costs to ensure a correct calculation of TCM. This information is vital for determining the cost of goods sold (COGS), which directly impacts a company’s profitability.

By understanding the formula and its components, businesses can effectively calculate their total cost of merchandise purchases and gain a clear picture of their inventory management. This knowledge empowers them to make informed decisions regarding purchasing, pricing, and overall financial planning.

Example for Clarity

- Include a numerical example to demonstrate the calculation of both goods available for sale and the total cost of merchandise purchases.

The Intricate Web of Inventory Management: Unraveling the Formula

In the world of accounting, inventory management is a crucial aspect for businesses to accurately track their merchandise and determine their financial position. One key component of inventory management is calculating the total cost of merchandise purchases, which involves understanding several key concepts.

Beginning Inventory: The Foundation

Inventory management begins with understanding beginning inventory, which represents the value of merchandise on hand at the start of an accounting period. It serves as the basis for calculating the total cost of merchandise purchases.

Tracking Purchases with Precision

Next, it’s essential to accurately record the cost of merchandise acquired during a period. This includes the purchase price, any applicable discounts, and any costs incurred to bring the goods to the store.

Transportation Costs: The Invisible Expense

Often overlooked, transportation-in expenses refer to the costs incurred to transport merchandise from the supplier to the business’s location. These costs, such as shipping and handling fees, must be included in the calculation of total merchandise purchases.

Ending Inventory: The Missing Piece

The ending inventory represents the value of merchandise still on hand at the end of an accounting period. It is subtracted from the goods available for sale to determine the cost of goods sold.

Goods Available for Sale: The Full Picture

Goods available for sale is calculated by adding the beginning inventory, purchases, and transportation-in expenses. This represents the total amount of merchandise available for sale during the period.

Calculating the Total Cost of Merchandise Purchases

Finally, the total cost of merchandise purchases is calculated using the following formula:

Total Cost of Merchandise Purchases = Beginning Inventory + Purchases + Transportation-In Expenses - Ending Inventory

Example for Clarity

Let’s illustrate these concepts with a numerical example. Suppose a business has the following information for a particular period:

- Beginning Inventory: $5,000

- Purchases: $12,000

- Transportation-In Expenses: $800

- Ending Inventory: $4,500

Using the formula, we can calculate the total cost of merchandise purchases:

Total Cost of Merchandise Purchases = $5,000 (Beginning Inventory) + $12,000 (Purchases) + $800 (Transportation-In Expenses) - $4,500 (Ending Inventory) = $13,300

This means that the business incurred $13,300 in total expenses to acquire the merchandise sold during the period. Understanding these concepts is crucial for accurate inventory management and proper financial reporting.